American Consumers Are Starting to Hit Their Breaking Point

American Consumers Are Starting to Hit Their Breaking Point

(Bloomberg Opinion) -- Signs are emerging that the resilience of American consumers is rapidly waning, potentially undermining one of the few remaining pillars supporting the bull market in equities.

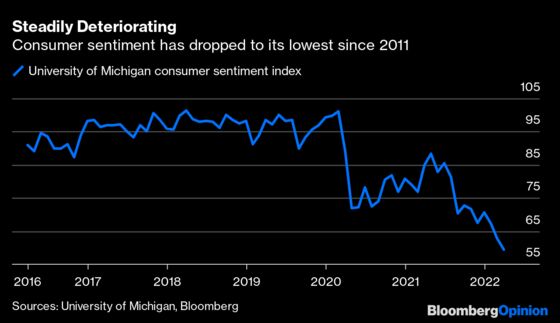

U.S. households have until recently mostly absorbed higher prices on everything from coffee to chicken to clothes, helping companies maintain fat profit margins despite higher input. But that doesn’t mean consumers were happy about paying more for the same goods, which is why the University of Michigan’s sentiment index has steadily deteriorated to the lowest since 2011.

The line from the bulls has been to watch what consumers do, not what they say. And for the most part, the bulls have been right about consumer spending, which is why many investors remain positive on stocks and the riskier parts of the credit markets. Although Americans have griped about higher prices, they have kept buying goods and have increasingly gone out to eat and started traveling as the pandemic waned.

But the latest surge in inflation rates, stemming in part from rising energy prices as a result of Russia's invasion of Ukraine, has pushed many households to the breaking point. Energy prices have surged about 26% over the past year while food costs have jumped 8% in the largest increase since 1981, according to Joseph Lavorgna, the chief economist at Natixis North America LLC. These two inputs account for more than 20% of household outlays, he wrote in a March 23 research note.

Meanwhile, the big increase in homes prices and the recent increase in 30-year mortgages rates to 4.5% from about 3% last year has pushed home loan payments as a percent of family income to 22.4% on average for new buyers from 18.7%, according to Tom Porcelli, the chief U.S. economist at RBC Capital Markets. Standard Chartered Bank strategist Steven Englander calculates that housing affordability is the lowest since 2007, with costs an estimated 15% higher in March than December.

Retail sales data have been resilient on a nominal basis, supported by inflation that isn't stripped out of the numbers. But a look at unit sales of general merchandise goods such as apparel, footwear, toys and sports equipment dropped in nine out of 10 weeks between the end of December and early March on a year-over-year basis, according to NPD Group data cited in a recent Wall Street Journal article. The report noted that 43% of consumers recently surveyed said they would delay less-important purchases if prices kept going up.

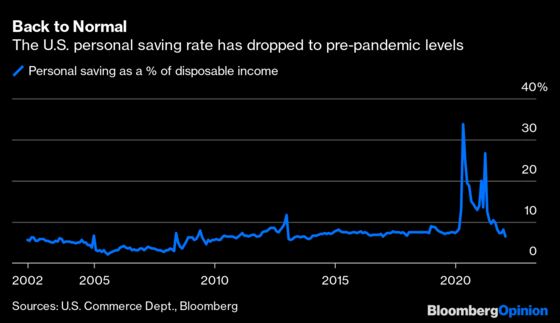

Analysts expect this trend to show up in Thursday’s personal consumption data, with the pace of increased spending expected to lag behind the inflation rate. It will also be important to watch the saving rate, which has dropped back to pre-pandemic levels. If the rate falls further, it may show that consumers are whittling down cash piles built up during the pandemic. Even if the rate stays the same, it may indicate that the days of profligate, pandemic-era spending are over.

The shift among consumers has been subtle, but one that has consequences amid the monetary and fiscal policy tightening that is currently happening. Consumer spending accounts for almost 70% of the annual economic output, up from around 60% in the early 1980s, the last time consumer price inflation was as high as it is now. The more consumers push back on higher prices, the bigger the ripple effect throughout the economy. Companies will see their profit margins shrink, diminishing their appetite to expand, invest or hire new people who are demanding substantially higher wages.

This isn't a reason to sell stocks or high-yield bonds outright. Many companies still have high cash balances and they have taken advance of buoyant credit markets in recent years to extend their debt maturities at historically low interest rates. But at the same time, the emerging weakness in consumer spending is enough to suggest that it's no longer safe to employ a “buy the dip” investing strategy like it was just a couple of months ago.

The longer consumers rein in their spending in response to the highest rates of inflation since the early 1980s, the more difficult it will be to emerge from the recession that seems increasingly inevitable. As we now know, recessions resulting from sudden exogenous shocks, such as the Covid-19 pandemic-induced on in 2020, can be reversed or offset extremely loose monetary policy and extremely generous fiscal policy. We may be about to find out that recessions born out of stagflationary shocks are harder to mitigate.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lisa Abramowicz is a co-host of "Bloomberg Surveillance" on Bloomberg TV.

Post a Comment