Buy votes, create disparity and divide people, that’s what democrat policies are designed to do. Joe Biden follows the playbook by cancelling $10k to $20k in student loan debt for those who have federal government loans. Students with private loans backed by the federal government are not eligible.

Additionally, Biden has extended the “COVID emergency payment moratorium” through the end of the year. No one with a federal student loan needs to restart paying until after the midterm election, in 2023. [White House Fact Sheet Here]

Additionally, Biden has extended the “COVID emergency payment moratorium” through the end of the year. No one with a federal student loan needs to restart paying until after the midterm election, in 2023. [White House Fact Sheet Here]

If the economy is doing so great, then why the need for bailouts?

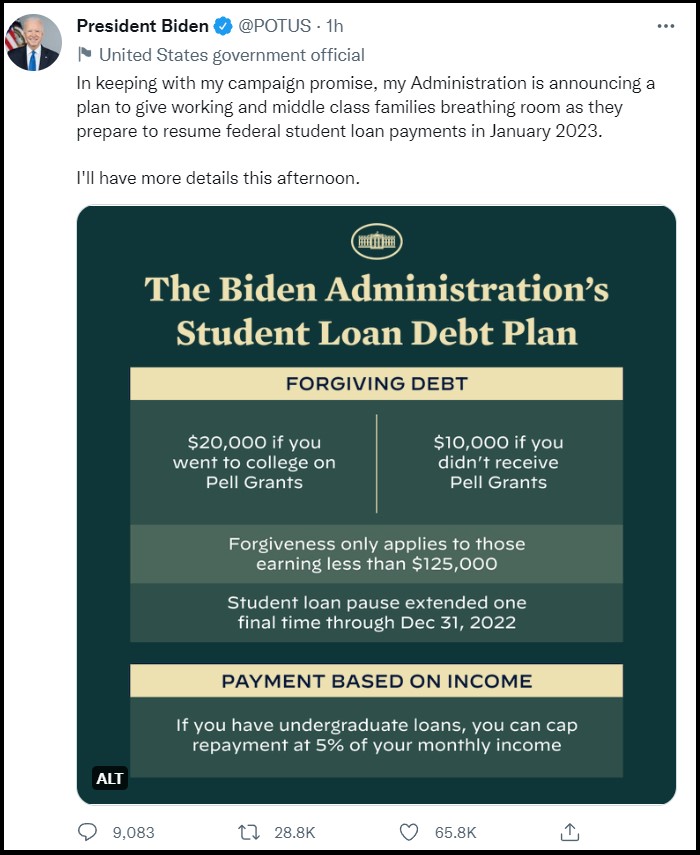

WASHINGTON (AP) — President Joe Biden on Wednesday announced his long-awaited plan to deliver on a campaign promise to provide $10,000 in student debt cancellation for millions of Americans — and up to $10,000 more for those with the greatest financial need — along with new measures to lower the burden of repayment for their remaining federal student debt.

Borrowers who earn less than $125,000 a year, or families earning less than $250,000, would be eligible for the $10,000 loan forgiveness, Biden announced in a tweet. For recipients of Pell Grants, which are reserved for undergraduates with the most significant financial need, the federal government would cancel up to an additional $10,000 in federal loan debt.

Biden is also extending a pause on federal student loan payments for what he called the “final time” through the end of 2022. He was set to deliver remarks Wednesday afternoon at the White House to unveil his proposal to the public.

If his plan survives legal challenges that are almost certain to come, it could offer a windfall to a swath of the nation in the run-up to this fall’s midterm elections. More than 43 million people have federal student debt, with an average balance of $37,667, according to federal data. Nearly a third of borrowers owe less than $10,000, and about half owe less than $20,000. The White House estimates that Biden’s announcement would erase the federal student debt of about 20 million people. (read more)